Perspectives

Non-alignment comes at a cost

May 2026

which have led in the past to world wars and which may again lead to disasters on an even vaster scale.”

- Jawaharlal Nehru, first Prime Minister of India, in September 1946

the goodwill of one partner or bloc.”

- Alexander Stubb, President of Finland, in March 2026

President Stubb delivered his words on Day 5 of the Strait of Hormuz blockade. Without a doubt, Nehru, one of the most seminal founders of the nation, would have beamed with satisfaction that India had consistently maintained this political philosophy for almost eight decades. However, as Stubb spoke, Qatari LNG cargoes bound for India were under force majeure, the Indian crude basket was on its way to $126 per barrel, and the Reserve Bank was drawing down forex reserves. The hazards of this consistent yet impractical policy were on full display yet again, throwing the Indian government and its population into a state of panic.

Following US-Israeli airstrikes that decapitated the Iranian leadership, the Revolutionary Guard closed the strait to commercial traffic, boarded vessels and laid sea mines across the shipping lanes. Within days, traffic had fallen to roughly 5% of its normal level, making it the largest oil supply disruption in the history of commodities markets.

India, with its insatiable thirst for imported oil and gas, was left exposed to the vagaries of other nation’s conflicts with non-alignment resulting in the need for hasty alliances and trades to secure supplies at any price. Oil and resource markets do not wait for war. They anticipate it. And when wars arrive, the countries most exposed are not necessarily those on the battlefield. Those that cannot control their inputs are invariably the most affected.

A Crude Reality

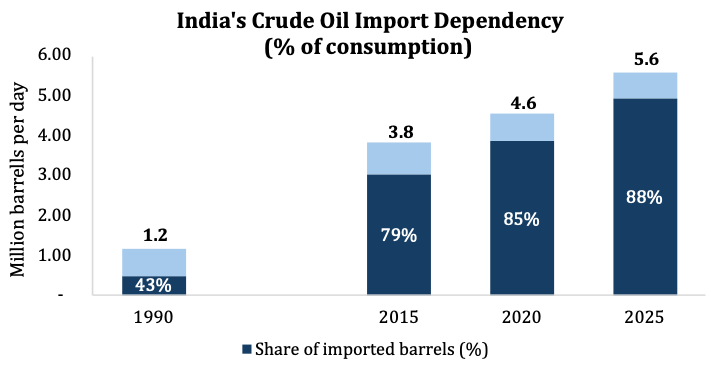

India’s dependence on imported crude oil is currently at an all time high at ~88% of current needs, as compared to 43% in 1990. Domestic production has fallen from ~0.64 million barrels per day in 1990 to ~0.58 million barrels per day in 2024. On the demand side, crude consumption has risen roughly 5x over the same period to 5.6 million barrels per day, making India the world's third-largest oil consumer. The result: oil imports have increased by 6.8% p.a. or 10x to ~5 million barrels per day. India has now surpassed China as the world's largest driver of incremental oil demand. The implication becomes easy for all to see: India is heavily dependent on external trading partners.

The correlation between oil and economic prosperity is swift and direct. Every $10 increase in crude widens India's current account deficit by 35-40 basis points, adds a similar quantum to inflation, and shaves 20-25 basis points off GDP growth. At $126 per barrel, these are not marginal adjustments. They are structural dislocations. The consequences arrived quickly. Forex reserves fell by approximately $30 billion in the three weeks following the conflict's escalation. The rupee weakened to a record low near Rs 95 against the dollar.

In 1991, after the Gulf War pushed oil above $40 a barrel, India's reserves fell to two to three weeks of import cover. Under cover of a general election, the Reserve Bank airlifted 67 tonnes of gold as collateral. The reforms that followed were not chosen. The pattern across India's economic history is consistent: the country absorbs the shock first and (hopefully) reconfigures afterwards. Though in the past several decades, the results have only been an increased reliance on imports rather than any modicum of self sufficiency.

Non-alignment combined with import dependence results in a structural vulnerability to economic shocks, directly felt by the populace. To stay in power, politicians would be well advised to amend this structural flaw with urgency.

Be Thy Neighbour

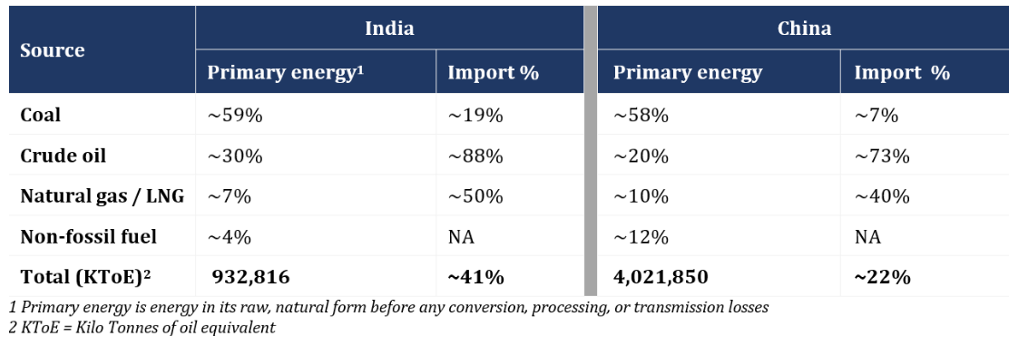

Import dependency runs deep across the energy basket. The Chinese experience is instructive and reflects poorly on India.

The import dependence gap between India and China is driven by two things: India's heavier reliance on crude, and a thinner non-fossil cushion, with non-fossil fuel only 4% of India's primary energy versus 12% in China. What makes the contrast even sharper is scale: China’s total primary energy supply is 4.3x India's, and yet its exposure to Hormuz disruption is structurally smaller despite being the world's largest energy consumer.

Supply chains play a role too: India’s imports are purely maritime in nature. Every barrel either arrives by ship or doesn't arrive at all. In contrast, China has built extensive but costly pipelines conveying oil and gas thousands of kilometres over land from Central Asia, Russia and Myanmar. It’s also diversified its sources with Russia catapulting to the top of China’s list of oil suppliers with no fear of retribution from foreign nations.

China is, by any reading, more non-aligned than India. Yet, it maintains trading relationships with a wide range of suppliers from around the world and dictates its own terms. This was a direct result of resource independence. Despite limited local resources, Beijing executed a massive renewables build-out and undertook huge investments into technology and infrastructure, all fueled by a vision to remain politically and economically independent.

What is India’s plan?

India's solar build-out is a genuine achievement. Solar capacity has grown fortyfold in a decade, and solar now accounts for close to 10% of total electricity generation. The caveat is one of denominators. Electricity accounts for roughly a fifth of India's total primary energy consumption. The balance, which includes transport, heat, industrial fuel, etc., runs entirely on imported hydrocarbons. The grid is greening. Yet dependency remains.

National Green Hydrogen Mission launched in 2023 with a ~$2.5 bn outlay and a target of 5 MT of capacity by 2030. As of late 2025, operational capacity stood at ~3% of the 2030 target. Out of 158 announced projects, 94% remain at the announcement stage. This potential solution threatens to underdeliver by an order of magnitude.

Nuclear tells a more promising story. The SHANTI Act, passed in December 2025, ended a 60-year nuclear prohibition: private companies can now directly own and operate reactors and the supplier liability under the earlier act has been eliminated. For the first time in six decades, the architecture for a serious build-out is in place.

The takeaway: India’s strides towards energy independence will take time. But political exigencies are immediate.

- Milton Friedman, Nobel Laureate in Economics and author of Capitalism and Freedom

In the autumn of 1955, Friedman arrived in New Delhi as part of an Eisenhower administration delegation, dispatched to offer a market-oriented counterweight to the socialist economists then shaping Nehru's Second Five-Year Plan. The meeting of minds, such as it was, resulted in no common ground.

In Nehru's worldview, capitalism was an evil; a scourge devoid of principles of nationalism and identity. He saw capitalism as imperialism's economic engine, and self-sufficiency through state planning as the only credible shield.

Seven years later, in Capitalism and Freedom, Friedman made the argument that economic freedom is not merely a complement to political freedom but its prerequisite. A society cannot long sustain one without the other. Nehru's India, he asserted, had chosen the wrong sequencing. It had pursued political non-alignment while building economic dependence into the foundations of the state.

The current crisis is a stress test, not a verdict. The reforms of 1991 transformed India's trajectory for a generation while opening the floodgates for imports and foreign investment. One hopes that the pressure of 2026 may prove similarly cathartic. There are signs, at least, that the crisis is being read correctly. Modi's recent alarming conservation appeal on foreign travel and gold purchases suggests a government that finally understands the import bill as a national security problem. India's trajectory remains one of the more remarkable of the modern era. What it has yet to build is the resource base that would make that trajectory irreversible.

The question is no longer whether the next disruption will arrive, but whether India chooses to build the factories, grids, and reactors that allow resource independence as prescribed by Friedman to enable political non-alignment as desired by Nehru. Otherwise, India will continue to negotiate, shipment by shipment, the costs of dependence, while receiving vacuous platitudes from equally affected heads of state.